he bank will need to become more flexible and reshape their business models to safely navigate the current period of volatility, achieve long-term growth and profitability.

First, it was the pandemic, and now, a combination of macroeconomic volatility and geopolitical disruption has upended many assumptions for global banks in 2022, including inflation, war, rising interest rates, and supply chain disruptions. However, one thing has not changed: valuation. In general, bank stock prices remain below other industries, reflecting the fact – as will be confirmed again in 2022 – that over half of global banks’ profits are below their cost of equity.

In this year’s Global Banking Annual Review, we carefully analyze the roller-coaster changes banks have experienced over the past few months, the increasing differences between banks of different countries and images, and the factors that make the best-performing banks stand out.

As businesses and governments increasingly commit to reducing greenhouse gas emissions, we also focus on sustainable finance, a hot topic in the banking industry. Despite persistent doubts and concerns about “greenwashing,” we find strong evidence that climate-related financing is entering the “next phase,” as the initial surge of funds for renewable energy gives way to deepening engagement with bank clients across sectors.

For banks, 2022 is a tumultuous year, full of shocks and uncertainties. The banking industry has rebounded from the pandemic with strong revenue growth, but the backdrop has changed greatly. Now, a series of interrelated shocks – some geopolitical, others the long-term economic and social impacts of the pandemic – are exacerbating fragility.

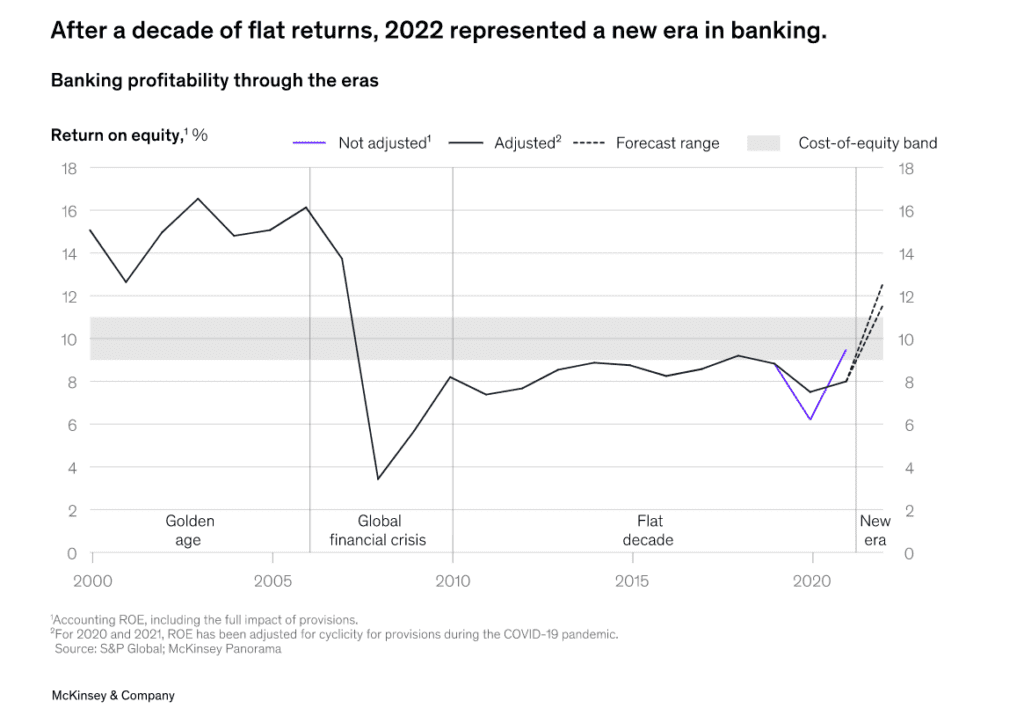

In 2022, bank profitability will reach its highest level in 14 years, with expected return on equity between 11.5% and 12.5% (see Table 1). Global revenue increased by $345 billion. The significant increase in net profit margin is driving this growth, as interest rates have risen after hovering near cyclical lows for many years. Currently, the Tier-1 capital adequacy ratio of the global banking system is 14-15%, the highest level in history.

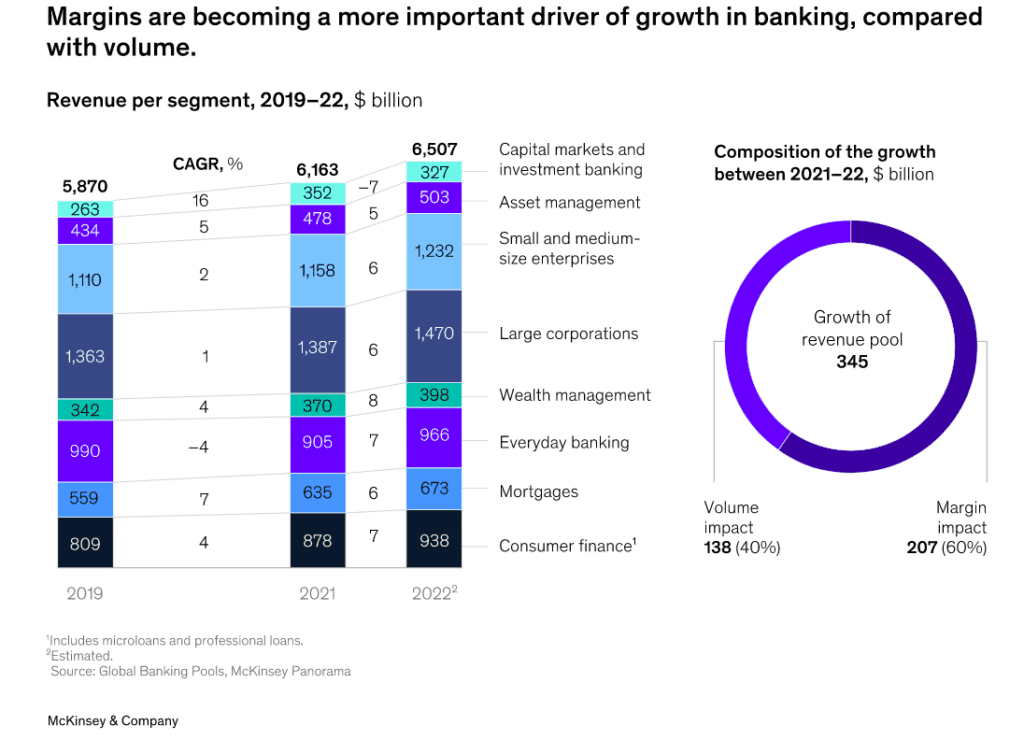

Improving profit margins accounts for 60% of income growth (Figure 2). Almost all areas of the banking industry experienced improvement except for capital markets and investment banking.

Nonetheless, more than half of the world’s banks will still have a return on equity lower than the cost of equity in 2022. Our analysis shows that, for the second half of 2022, only 35% of global banks achieved a return above the cost of equity through improving profit margins. Less than 15% of banks had a return that exceeded their respective cost of equity of 4%.

The aftermath of COVID-19 and geopolitical tensions are disrupting the financial industry. The persistent long-tail effects of the COVID-19 pandemic, along with the escalating tensions between Russia and Ukraine and Taiwan in February 2022, signal the brutal return of geopolitics as a disruptive force. The resulting five impacts are affecting the global banking industry:

Macroeconomic impact. The soaring inflation rate and the possibility of a recession are a severe test for central banks worldwide, although they are trying to control quantitative easing policies.

Asset price shock. This includes the sharp decline in the Chinese real estate market, the sharp devaluation of financial technology companies and cryptocurrencies, and the bankruptcy of some high-profile crypto institutions.

Energy and food supply shock. Energy and food supply disruptions related to the Ukraine conflict are exacerbating inflation and endangering the livelihoods of millions of people.

Supply chain shock. Supply chain disruptions continue to affect global markets during the first pandemic lockdown.

Talent shock. Employment underwent significant changes during the COVID-19 period, with people changing jobs, working remotely or exiting the workforce entirely.

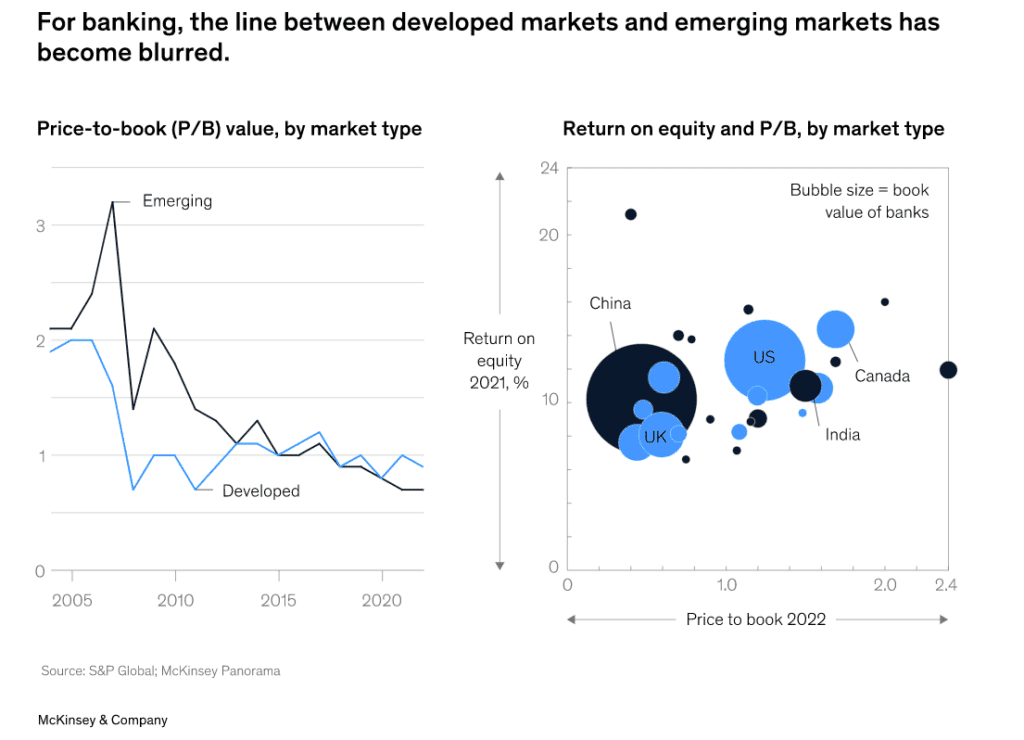

The consequences vary by region and within regions, particularly in emerging markets. A notable feature of this period is that some banks in some regions are growing strongly, with profits and revenues increasing. This more optimistic picture can be found in specific markets – for example, many regional banks in the United States and Canada’s five largest banks. The largest banks in emerging economies, such as India, Indonesia, Mexico, and South Africa, are performing very well.

This is not the typical dichotomy between emerging and developed economies. In fact, it can be said that at least in the banking industry, the entire concept of “emerging markets” died this year (Figure 3). The countries it referred to are no longer a homogenous bloc: some of the best-performing high-growth banks are in Asia, and some of the worst-performing low-growth banks are also in Asia.

With the economic slowdown, the divergence between banks will further widen

The uncertain macroeconomic outlook will affect banks in two different ways, albeit to varying degrees. First, as interest rates rise, profit margins may continue to improve, but this could be temporary. Second, banks face a long-term growth slowdown. The result of these pressures will be an increase in the trend we noted last year of “big dispersion” between banks, with significant variation depending on funding conditions, geography and operating models.

Two economic scenarios: How bad (or good) could they be for banks? We simulated the impact of two possible macroeconomic scenarios on banks: inflationary growth and stagflation. Whichever the case, we expect the initial stage to be positive for banks. Rising rates will increase net interest margins, as the repricing of short-term lending products, such as consumer finance, is faster than for liabilities. The global banking industry’s revenue could grow 5% to 6% in 2022.

At this stage, both scenarios predict that costs and risks remain under control. The global banking industry’s return on equity will rise to around 12% in 2022, two percentage points higher than in 2021.

The biggest question is what will happen in the transitional phase of deteriorating economic growth, which is when the full impact of the scenarios will start to play out. Banks may experience three effects – slower business growth, rising costs and rising delinquency rates – which could be large or small depending on the circumstances.

The story of divergence will continue to play out in these scenarios. Banks in the Asia-Pacific region may benefit from stronger macroeconomic prospects, while those in Europe may see the full impact of this situation sooner and experience more adverse effects. If there is long-term recession, we estimate that the global return on equity may fall to 7% by 2026 – return on equity for European banks will be lower than 6%.

The net effect may be further concentration of growth in emerging Asia, China, Latin America and the US. We expect these regions to account for about 80% of the estimated $1.3tn growth in global banking industry revenue for the period from 2021 to 2025.

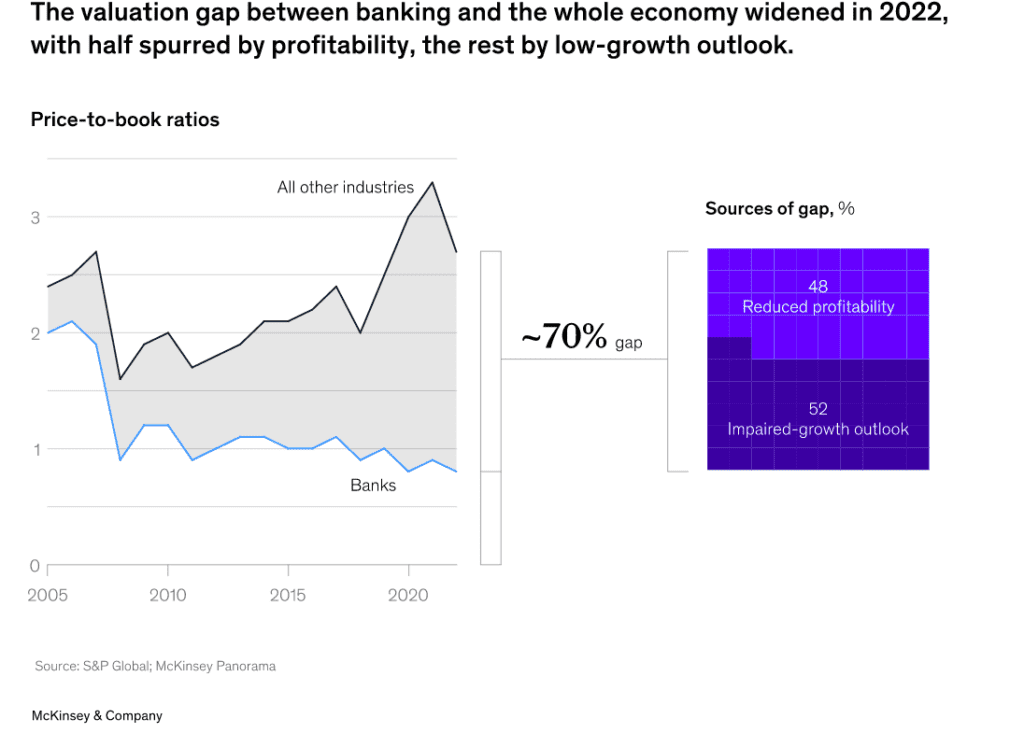

What does not change is that bank trading prices are increasingly discounted compared to other industries The valuation of the banking industry as a sector is far lower than other industries, reflecting the severe challenges faced by traditional banks. About half of all banks are net destroyers of value, while many others are weighed down by slow growth and low profit expectations.

Total global market cap peaked at $16tn in 2021, falling to $14.5tn by May 2022. Half of this valuation is represented by traditional bank institutions, while experts and fintech firms represent the other half – this ratio was 30% five years ago.

The valuation gap between traditional banks and fintech firms still remains significant, even with the slump in cryptocurrencies and buy-now-pay-later in 2022, which resulted in dropouts in fintech valuations.

Among the valuation gap between the banking industry and other industries, only about half reflects the low-profitability of the banking sector (Figure 4). The other half reflects the expectation of a lack of future growth, which is proven by the banking industry’s low price-to-earnings ratios (P/E ratios). The banking industry’s P/E ratio is around 13x, while the average P/E ratio for other industries is 20x.

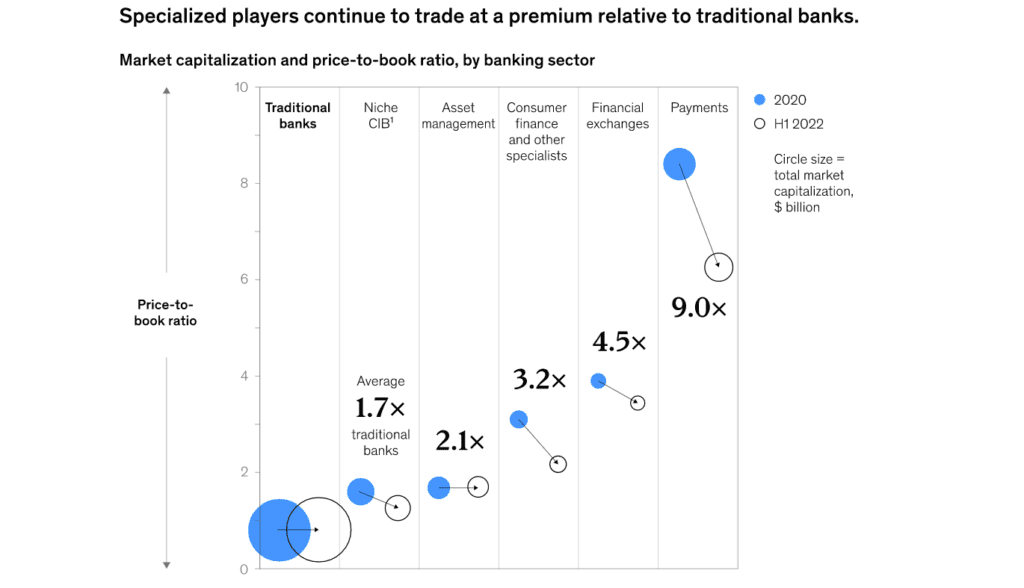

In this overall bleak picture, there are also some bright spots. Globally, about 15% of banks meet the “North Star” criteria. They have high price-to-earnings ratios, indicating high expectations for long-term growth, and high price-to-book ratios, reflecting their short-term profitability adjusted for risk. Their valuations are two to five times higher than other banks. Most of these banks are experts in commercial models. They are more geographically diverse and focus on certain industries; for example, payment providers in North America and consumer finance and other specialized companies from emerging markets in Asia have shown high growth and profitability.

In last year’s bank evaluation, we found that about half of the banks were value destroyers. This year, by focusing not only on profitability but also on growth rates, we found that, in addition to this 50%, 35% of companies are currently creating value but do not have enough growth to ensure that they will continue to do so. These banks have high price-to-earnings ratios but low price-to-book ratios. In other words, they are profitable now, but long-term expectations for future growth are not optimistic.

Bank performance varies by region, specialization, customer segmentation, and scale. To understand why and how banks have ultimately achieved their current level, we have studied them from four dimensions: geography, specialization, customer segmentation, and scale.

Geography is a key factor. We analyzed the deviation of banks’ price-to-book ratios over the past decade and estimated the key driving factors behind the change using a standard regression model. Geographic location is one of the key factors in banks’ valuations. Overall, we found that a bank’s primary location accounts for 68% of its valuation, a proportion that has continued to rise since 2014.

Last year, many European banks were no longer profitable, and in 2021, only 25% of the valuations of the top 300 European banks were higher than their book values. In the coming months, they will face even greater pressures from potential recessions. In contrast, about 25% of the market value of emerging Asian banks is 1.5 times or more than their book values, partly due to rapid economic growth and their innovative approaches. In the Middle East, Latin America, and North America, net asset returns and net asset revenue ratios are also high.

Specialization can be profitable. It is not surprising that high-valuation specialized players and fintech companies are active in bank products that generate profits, including deposits, payments, and consumer finance. The result is a two-speed system, with traditional banks lagging behind (Table 5). Overall, the banking system destroyed about $12 billion of economic value in 2021, with a return on equity that failed to match its cost of capital. However, there is a wide range of divergences in all areas of banking specialization.

It is necessary to re-examine customer segmentation and demographics. Our analysis indicates that disproportionate revenue is often locked in specific segments in the retail banking industry. A significant feature of this analysis is the gap between population distribution and age at which they generate bank revenue. For example, in the US, bank revenue peaks in the age group of 60-70, which is approximately 40 years after the population peak. In China, the trend is precisely the opposite: revenue peaks 20 years earlier than the population peak.

Size matters. About 70% of market capitalization is held by banks with a P/B ratio of over 1 (about half of all banks), even though they only hold 30% of assets. Among these banks, only 10% have achieved scale, representing at least 10% of market share; the rest of these “value-creating” banks can increase their size through mergers and acquisitions.

Double challenge: managing the present while preparing for the future. Over the next five to ten years, market pressures and changes – including technological disruption to traditional banking – will lead to fundamental structural disruption. Banks need to improve their short-term resilience and make long-term investments to innovate and prepare for future profitability, growth, and higher valuations.

In the near term, four strategic objectives can help strengthen resilience:

Financial flexibility. The best-performing banks have a net-profit structure with low sensitivity to interest rates and risk costs. Their target cost-income ratio should be between 35% and 40%. Business recovery. This means reducing or eliminating a presence in high-risk countries and establishing exceptional risk management practices. Digital and technological resilience. Cyberattacks remain a significant risk. The best banks have well-protected technological infrastructures and excellent data security. Institutional resilience. The best-performing banks will have a fast response time and invest in attracting, retraining, and retaining the best talent.

From a longer-term perspective, banks need to transition from traditional business models to more future-proof platforms, possibly by decoupling daily banking operations from complex financing or advisory business units. Banks can consider several approaches. For example, they can cultivate highly differentiated customer relationships, with a focus on building deep emotional connections. They can also develop proprietary insights on data and customer groups, including using advanced analytics. A third option is to make substantial and clear bets when allocating resources and capital. Fourth, banks can create new customer channels and revenue streams, such as subscription fees, payment fees, and distribution fees, which do not involve the balance sheet. Banks can focus on innovation, with the goal of instilling a genuine entrepreneurial culture and attracting the talent needed to make contributions in that culture. Finally, as described in the next section, banks can formulate a strategy for environmental transformation.

Sustainable finance has become an important component of banking business

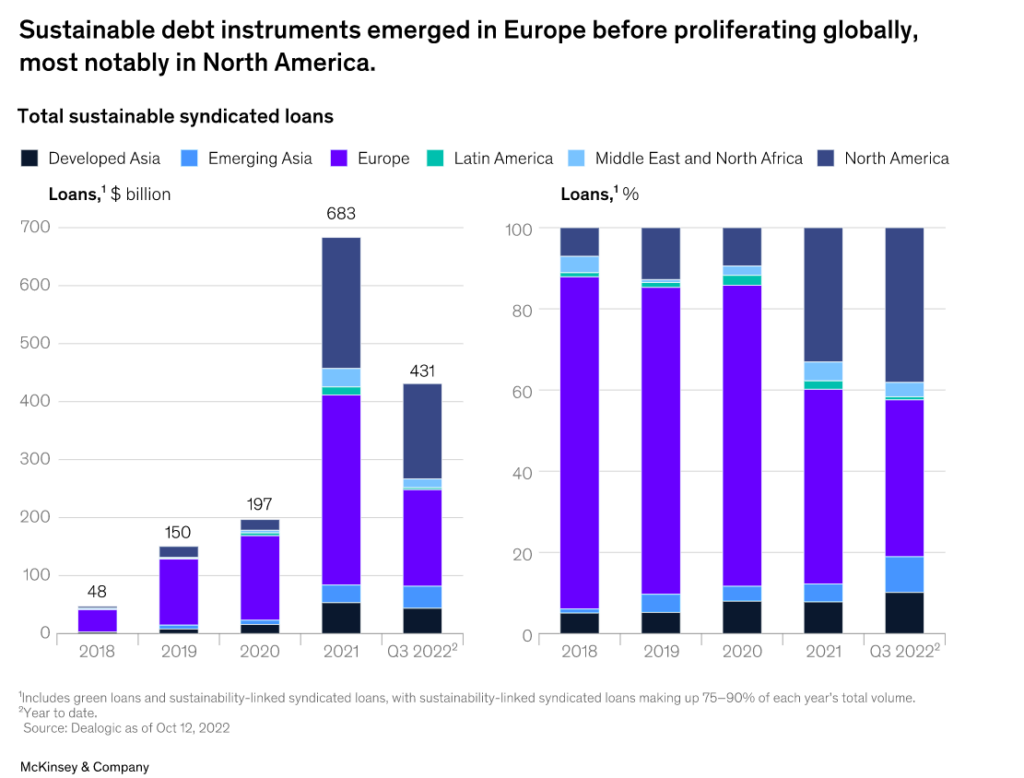

Five years ago, the issuance of sustainable debt instruments was close to zero, but by 2021, their issuance is expected to increase significantly year-on-year. The issuance of sustainable debt instruments, including green bonds, sustainable development bonds, social bonds, and sustainable development-linked bonds, is expected to reach US$965 billion, up 80% from 2020. The volume of sustainable loan syndications, including green loans and sustainable-linked loans, is expected to reach US$683 billion in 2021, up by more than 200% from 2020. Sustainable financing activities related to capital markets, including mergers and acquisitions, shares, and carbon trading, have also expanded in recent years.

In 2022, this momentum slowed down amid a broader market decline, but sustainable debt capital markets and loans performed better than the overall debt market. The issuance of sustainable bonds currently accounts for about 12% of the total bond market, while sustainable-related syndicated loans account for about 13% of the total global syndicated loan volume.

As sustainable instruments are being accepted, scrutiny of how they are labeled is also increasing. In particular, loans and bonds linked to sustainability need to establish credibility. More broadly, there is a need to disaggregate into environmental, social, and governance categories to distinguish climate financing and track it separately.

Green bonds initially dominated the sustainable debt market but have been replaced by performance-based sustainable-linked loans that link interest rates to established sustainability targets. Challenges remain in setting targets, including rewards for achieving established targets and punishments for failing to meet them.

Europe has traditionally led the way in sustainable debt instrument issuance. In 2018, the region accounted for over 80% of sustainable loan syndications, but at the same time, North America’s market share continues to grow.

The financing of clean energy projects reached a new high in 2021 at $164 billion, with $77 billion coming from solar projects. However, in the first half of 2022, the financing amount from banks for clean energy projects dropped by 38%, mainly due to the decline in solar and wind projects. Nevertheless, the continued growth of clean energy project financing is expected to narrow the gap between the amount needed for renewable energy generation and energy transition.

Competition for clean energy financing is also becoming increasingly intense as various well-funded participants enter the market. In 2021, private equity firms invested $76 billion in renewable energy, sustainable mobility, and carbon technology fields, more than doubling the amount invested in 2017. During the same period, venture capital firms invested almost twice as much in the same technology.

As transitional technologies such as solar and wind mature, developers are adjusting their bidding methods to consider different risks and contract durations. Therefore, banks must make changes by shortening loan terms, integrating project portfolios to increase ticket size, and playing a structural role to earn incremental fees. Banks are also beginning to explore emerging technologies such as hydrogen and storage.

Entering a New Era In the next transition era, we will continue to focus on capital allocation required for low-emission power generation and many new aspects of global energy transition as a priority for financing. These new initiatives include growth electrification, energy transmission and distribution infrastructure construction (including grid-scale storage), emissions reduction of high-emitting and energy-intensive sectors such as steel and cement, and natural climate solutions.

Signs of the next era are already visible. In addition to continuing to invest in power generation, it also includes increased investment in emerging technologies such as hydrogen and grid storage, as well as innovation by banks aimed at financing low-carbon transitions. Leading global banks and smaller local banks are developing new products and platforms, and in some cases, independent financing entities spanning industries.

Policy shifts, new technologies, and increasing corporate momentum are driving economic growth. Therefore, banks are shifting from basic understandings of baselines to exploring levers with customers to achieve financing and reduce emissions in the real economy.

Government subsidies, tax credits, and guarantees, among other interventions, are unlocking bankable value pools to enable the low-carbon transition. In the United States, for example, extensions of and changes to tax credit programs under the Inflation Reduction Act could almost double new solar and wind capacity by 2030.

Technological innovation is reducing costs while improving preparedness. For example, the cost of lithium-ion batteries has fallen by 97% since 1991, promoting the adoption of electric vehicles. According to estimates from the McKinsey Future of Mobility Center, bank loans for electric vehicles have almost doubled since 2017 and are expected to grow 24% annually, exceeding $800 billion by 2030.

Companies are shifting from commitments to actions to accelerate decarbonization. Some companies initially provided funding for pilot projects and initiatives through their own balance sheets, but many are now seeking banking institutions and capital markets to provide funding for larger-scale operations and strategic initiatives. For example, H2 Green Steel, a Swedish steel company, recently announced €3.5 billion in debt and equity financing support from European financial institutions to build a sustainable hydrogen-powered “green” steel plant in Sweden.

Regulatory agencies are focusing on the climate and sustainable development. Regulations and standards focusing on disclosure will increase the rigor and transparency of climate financing and create more potential for banks to identify financing opportunities. For example, in March 2022, the International Sustainability Standards Board (ISSB) issued a global climate-related and sustainability-related disclosure standards draft. The European Union and the United Kingdom have also proposed new reporting requirements.

Banks’ untapped value pool By 2030, net-zero transition funding needs may exceed $4.4 trillion annually. McKinsey estimates that banks are at the forefront, providing financing and consulting support for a variety of opportunities. For example, by 2030, clean power investment needs to triple from 2020 levels, while road transport electrification investment needs to increase tenfold from 2020 levels by 2030.

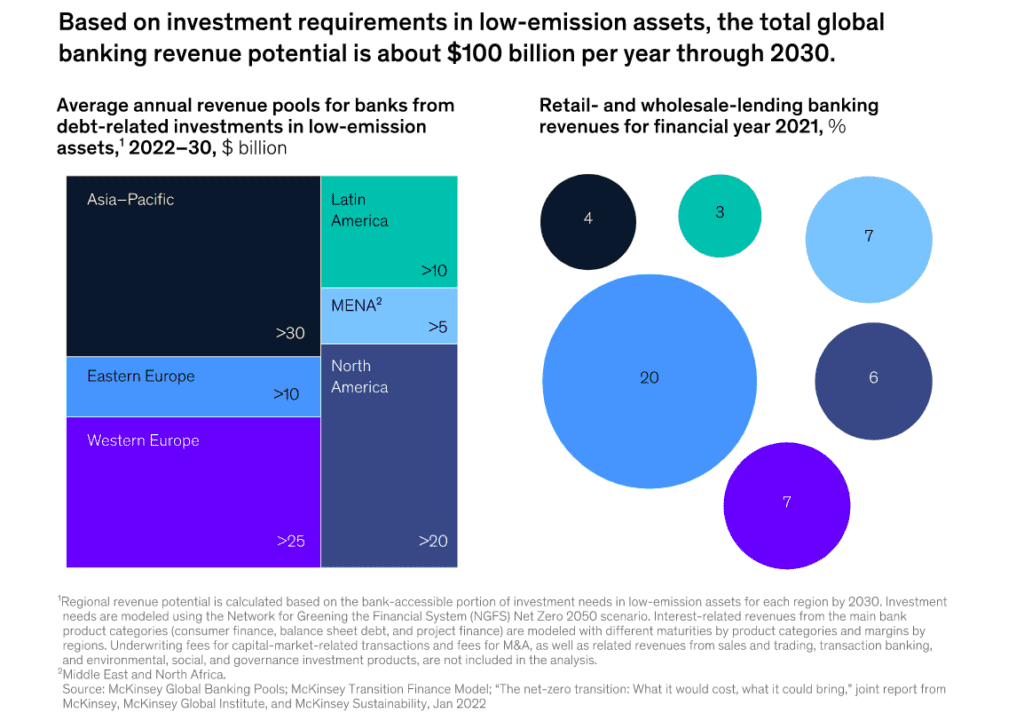

Based on this McKinsey model, we estimate that commercial financial institutions have approximately $820 billion in direct financing opportunities each year. In addition, banks can provide an additional $1.5 trillion in investment for businesses between 2021 and 2030.

We estimate that by 2030, banks’ revenue potential for debt investments in climate financing will average about $100 billion annually. This represents about 5% of the global banking industry’s total revenue pool.

Leading the Next Era of Climate Finance

Banks interested in financing the transition to clean energy need to fully understand the challenges they must overcome. They can also study early successful experiences and develop roadmaps based on their strengths and goals.

Balancing Challenges In the next era, the following challenges will be significant:

Project Economics. The longer-term returns of certain technologies may increase risks and reduce returns, while the upfront investment required for cross-sector transition may make lenders hesitant to invest capital. Market Conditions. Profit margins for some profitable technologies, including solar, have been shrinking. Credit Risk. Currently, many deals are not within the risk appetite of banks due to lack of historical performance data, price uncertainty or regulatory dependence leading to future cash flow uncertainty, long tenures, unconventional legal structures, or loans to new or small companies. Scalability. Many green projects are dependent on permits, supportive infrastructure, and supply chains, which can delay scaling. Standardization and Disclosure. There are currently no established standards for sustainability-related financial products or performance metrics. Reputation Risk. Financing the brown-to-green transition may cause reputational issues considering the situation of clients such as fossil fuel companies.

Paving the Way Banks will need a flexible approach to assess the rapidly changing sustainable finance market. Different types of institutions have different experiences.

Companies and Investment banks have made the most progress, but there are still many opportunities. Building on the progress of renewable energy in the past decade, banks can expand their financing abilities to fill the gaps in solar, wind, and hydropower while developing capabilities for new clean energy such as green hydrogen. They can seize the opportunity for transition financing of their existing customer base and expand their advisory capabilities to support customers.

Commercial and Small Business banking. Banks can provide equipment financing for energy-saving measures or funding for renovations as customers revamp their buildings and change their energy mix. As companies transition to electric and fuel cell vehicles, they can also provide fleet financing.

Retail banking can provide financing solutions for retrofits, home appliances, and rooftop solar panels. Additionally, they can seize the huge opportunity in auto finance from the adoption of electric vehicles.

Wealth and Asset Management can develop thematic investment choices, targeted climate forward investment papers to meet the needs of institutional and retail investors. Financial institutions and retail investors are increasingly shifting their attention from general ESG themes to low-carbon transformation.

Banks have been undervalued compared to other industries even before this year’s macroeconomic disruptions and geopolitical turmoil ended over a decade of relative stability. This pattern is set to continue in 2022 – unsurprising given that the majority of the world’s banks have earnings below cost of equity.

The overall pattern obscures the success of banking groups in regions such as the US, Canada, India, Indonesia, and Mexico. Studying these banks can provide insights into the conditions associated with high performance.

Additionally, banks’ vision extends beyond short-term profitability. Most noteworthy is the evidence that the initial surge in renewable energy funding opened the door to deeper engagement with cross-sector banking clients.